Rethink Benefits for a Working Crew

Reduce healthcare costs, spend less time managing benefits, keep crews healthy and working, and provide benefits that help attract and retain great employees.

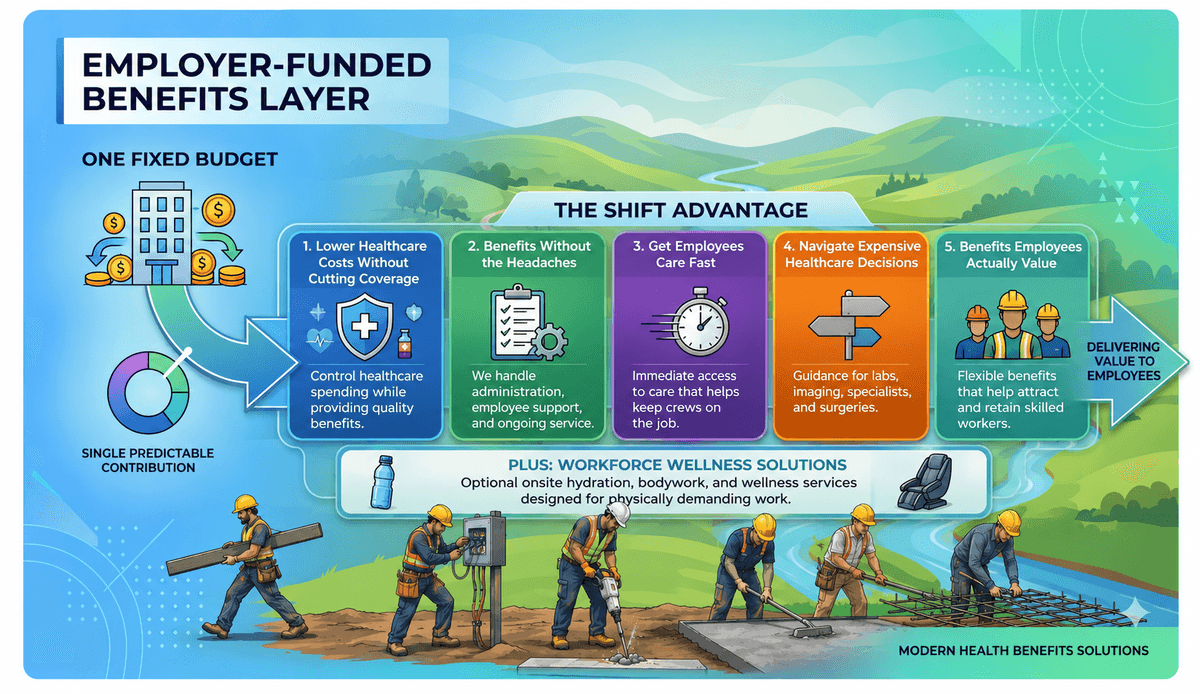

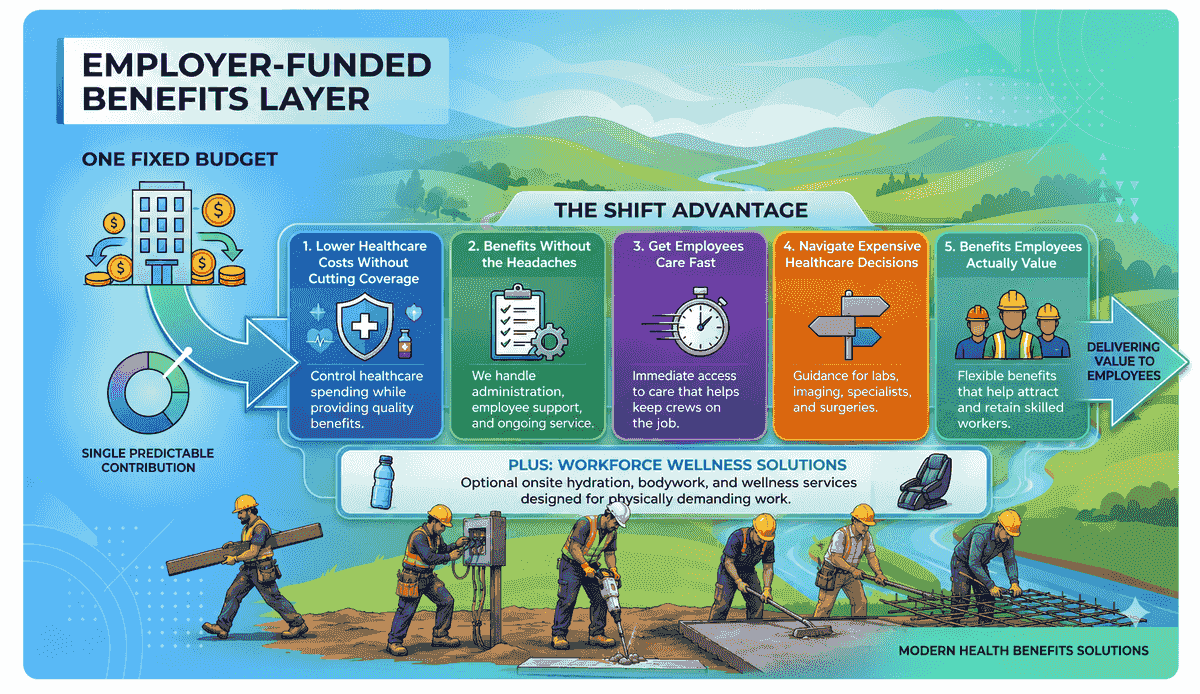

How It Works

Fixed Allowance Coverage

ICHRA is Group sponsored, ACA compliant, tax free, defined contribution coverage that uses the individual market.

HSA Plans

Tax free dollars that can be used on a wide range of medical expenses. Now more flexible than ever.

AI Driven Virtual Care

Instant care that saves your workers from a day off work.

Onsite Bodywork & Health Kits

Fix the aches that come with the job- right on site.

Stay hydrated for better performance.

Tool & Gear Stipend

Turn you savings into better boots, tools, and gear- your crew chooses.

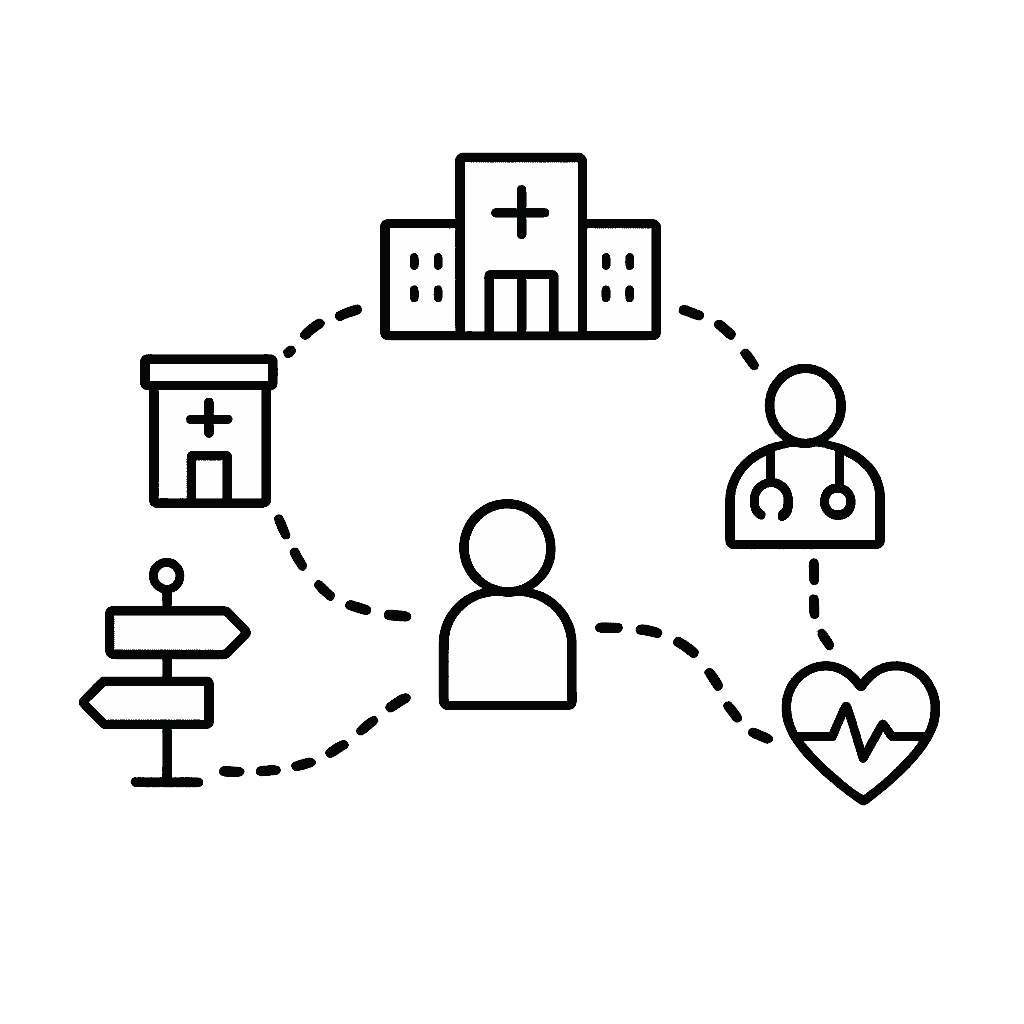

Concierge Style Care Navigation

No wrong turns. No surprise bills. We guide your people to the right care.

Early Results from Employers Using Shift

Life Design Build was offering their employees a stipend to buy their own health coverage.

They implemented an ICHRA, which essentially turned a $500 / month stipend into $650 of spending power with the tax savings.

Indian Creek faced a 18% rate hike at renewal.

Shift helped actually cut their existing spend by 26% and added more choice in plans.

Owner/GM Tyson Jacobs says working with Shift is easy and he appreciates the fast response to issues.

Guardian Partners offered a Kaiser group plan.

But when they started expanding to new locations not served by Kaiser they ran into a problem.

Shift implemented an ICHRA for a "new hire" class only, allowing current employees to keep Kaiser and new ones to get a plan that offered providers in their area.